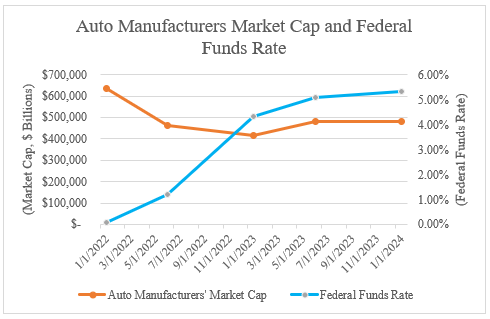

The automotive industry typically performs well when consumer confidence is high and when interest rates are low. I decided to test this idea over the past two years because during this time, we’ve experienced a significant rise in interest rates.

To do so, I tracked the total market capitalization for the top five auto manufacturers as a proxy for automotive industry performance, and the Federal Funds rate, which broadly impacts interest rates, for the time period between January 1, 2022 and January 1, 2024.

As predicted, based on this limited data, it appears that auto industry value has declined as interest rates have risen. The chart below shows that this correlation does not seem to continue as interest rates become more stable in 2023. This seems to indicate that investors might react to large changes in interest rates, but that more modest increases, coupled with signs from the Fed that interest rate hikes are starting to slow, might not impact auto manufacturers’ stock prices as heavily. It is important to note, though, that the total market cap for auto manufacturers begins to recover in 2023, but not to 2022 levels—as interest rates remain at historically high levels throughout 2023.

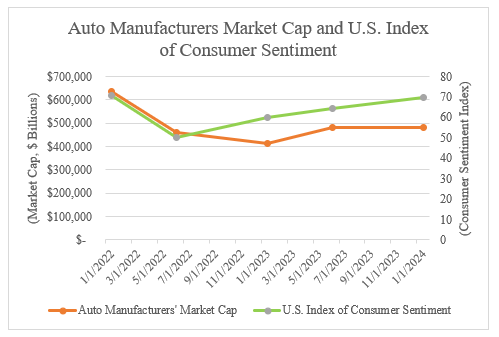

There appears to be some correlation between auto industry value and U.S. consumer sentiment (measured by the U.S. Index of Consumer Sentiment) over the past two years, but only in the first half of 2022 as shown in the chart below:

However, the Consumer Sentiment Index has averaged 85 between 1952 and 2024. Therefore, consumer confidence was below average over the past two years while the auto manufacturer market cap was generally deflated. In this context, the data still seems to support the correlation between auto industry performance and consumer confidence.

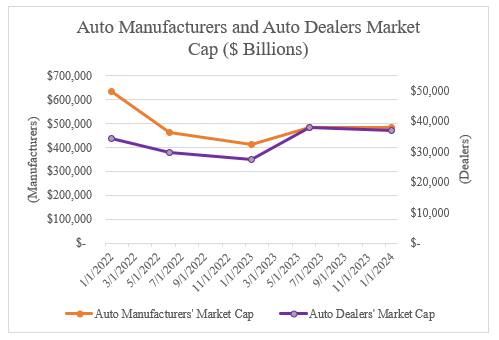

Since consumers are more directly impacted by auto dealers, as opposed to auto manufacturers, it is relevant to track the market cap for dealers as well. As shown below, the market cap for auto dealers (measured by the top six public auto dealers) has generally fluctuated in line with car manufacturers over the last two years.

The limited data presented in the charts above appears to support the idea that the values of auto dealers and manufacturers are impacted by changes in interest rates (negative correlation) and consumer confidence (positive correlation). However, it is important to note that many other macro- and micro-economic factors impact these metrics. In addition, a change in one metric could take time to impact another metric; there is likely a lag in the correlations over time. Therefore, while it is interesting to observe these potential correlations over the last two years, they should not be viewed as a rule to estimate future changes.

Schneider Downs has significant experience in preparing business valuations of car dealerships and a range of private businesses for various purposes including gift/estate taxes, buy/sell purposes and financial reporting. Please contact Steve Thimons (412-697-5281; [email protected]) or Thomas D. Pratt (412-697-5615; [email protected]) for more information about Schneider Downs’ business valuation services.

Data Sources:

Macrotrends

Companies Market Cap

Yahoo Finance

FRED, Federal Reserve Economic Data

YCharts

About Schneider Downs Business Consulting

Schneider Downs Business Consulting delivers sophisticated consulting services to meet the complex needs of today’s business environment. Our team features experienced professionals across a diverse array of specialties that allows us to help our clients make more informed business decisions across every facet of their operations.

To learn more, visit our dedicated Business Consulting page.