With the Federal Reserve (Fed) starting its interest rate-cutting cycle, the question many homebuyers face is “How will this affect my mortgage rate?” While the Fed does not explicitly set the federal funds rate, the Federal Open Markets Committee, a subset of the members of the Federal Reserve, sets the federal fund rate.

The federal funds rate is the interest rate banks pay to borrow money from each other overnight. When the Fed wants the rate to go up, they sell government bonds and buy government bonds when it wants the rate to go down.

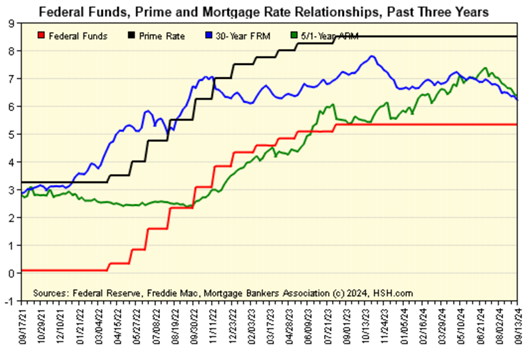

The Federal Reserve has kept the federal funds rate in a range of 5.25% to 5.5% since July 2023. To combat inflation, the Federal Reserve took interest rates from 0% during COVID to the current level. With the recent 50-basis point reduction in the target federal funds rate, the new target fed funds rate is 4.75% to 5%. Before the Federal Reserve raised interest rates in 2022, this rate hadn’t gone higher than 2.25% since 2008. While the level of interest rates has hovered near zero for much of the last decade, it rose above 19% in the early 1980s under Paul Volcker as the Fed tried to get runaway inflation under control. As the chart below illustrates, while interest rates are high when compared to recent times, historically they are still relatively in line (or lower) when put into historical context.

The typical effect of an interest rate cut is that variable-rate mortgages, including home equity lines of credit (HELOCs) and adjustable-rate mortgages (ARMs), will see rates decline. Those variable rates are tied to what is known as the prime rate, the interest rate banks charge their most creditworthy customers, which is directly influenced by the fed funds rate. While not always the case, in most cases, the fixed rate mortgage rate would likely move down as well. The chart below shows the relationship between the federal funds rate, the prime rate, the 30-year mortgage, and a conventional 5/1 mortgage ARM (adjustable-rate mortgage).

While prevailing sentiment may be for long-term mortgage rates to come down as the Federal Reserve starts their rate cutting cycle, this is not a guarantee. Mortgage rates can and will respond to many economic signals besides the federal funds rate. While the Federal reserve can have a heavy influence on where mortgage rates result, there are also many other factors to consider such as inflation, the health of the economy, investor appetite for mortgage bonds, and personal credit history, to name a few. If you would like to learn more about where current mortgage rates sit, please reach out to a local mortgage broker or banker to receive up to date estimates.

Source: How The Fed Affects Mortgage Rates – Forbes Advisor

Schneider Downs Wealth Management Advisors, LP (SDWMA) is a registered investment adviser with the U.S. Securities and Exchange Commission (SEC). SDWMA provides fee-based investment management services and financial planning services, along with fee-based retirement advisory and consulting services. Material discussed is meant for informational purposes only, and it is not to be construed as investment, tax or legal advice. Please note that individual situations can vary. Therefore, this information should be relied upon when coordinated with individual professional advice. Registration with the SEC does not imply any level of skill or training.