“Bean counter” is a colloquial term sometimes used to describe an accountant focused on minor details. When it comes to forensic accountants tracing commingled assets, maybe we should be called “red and green bean counters.” Here, the red beans represent tainted or illegally obtained assets, while the green beans represent untainted or “clean” assets obtained through lawful means.

Tainted assets can include the proceeds from a wide variety of criminal activities, such as selling an asset pledged as collateral without the lender’s consent, a fraudulent investment offering or insurance claim, a Ponzi scheme, or an embezzlement from an employer.

The differentiation between tainted and untainted assets can become important when it comes to situations like criminal or civil asset forfeiture and determining assets available for creditors related to a bankruptcy. This differentiation can become complicated when assets are commingled and not specifically identifiable.

As pointed out in William Stoddard’s widely cited 2002 Nevada Law Journal article Tracing Principles in Revised Article 9 § 9-315(B)(2): A Matter of Careless Drafting, or an Invitation to Creative Lawyering:

“The goal of ‘tracing’ is not to trace anything at all in many cases, but rather serves as an equitable substitute for the impossibility of specific identification.”

In U.S. v. Henshaw, the Tenth Circuit of U.S. Court of Appeals indicated that the district court properly turned to equitable tracing principles and stated, “There are several alternative methods, none of which is optimal for all commingling cases; courts exercise case-specific judgment to select the method best suited to achieve a fair and equitable result on the facts before them.”

Four widely accepted methods of tracing commingled assets include (1) first in, first out (FIFO); (2) last in, first out (LIFO); (3) lowest intermediate balance rule (LIBR); and (4) pro rata distribution. Most accountants are familiar with FIFO and LIFO from inventory pricing methods, but LIBR and pro rata distribution methods are also available.

To show these methods in action, I’ve created examples below leveraging red and green beans to represent tainted and untainted commingled assets. The red beans represent tainted or illegally obtained assets, and the green beans represent untainted or “clean” assets obtained through lawful means. Each of these examples follows the same fact pattern, adding a total of 38 beans in equal proportions and removing 26 beans, but each method ends with different results for the number of red and green beans removed and remaining.

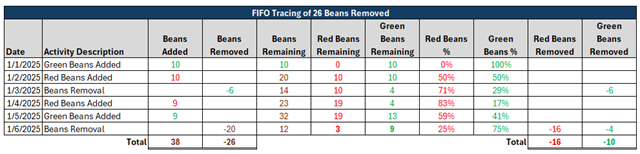

First in, First Out (FIFO)

The FIFO method assumes assets removed are traceable to the earliest assets added into a commingled account. The oldest assets are removed before newer assets. The first assets added are the first removed.

For the below FIFO example, you will see the first addition of beans being 10 green beans. Since those are the first beans added, the first beans removed are all green beans. It is not until those first 10 green beans are all removed on January 6 that all of the red beans added on January 2 and some added on the 14th are removed.

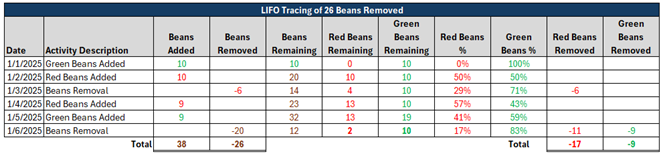

Last in, First Out (LIFO)

The LIFO method assumes that assets removed are traceable to the most recent assets added into a commingled account. The newest assets are removed before more stale assets. The most recent assets added are the first removed.

For the below LIFO example, you will see the last addition of beans before the first removal being 10 red beans. Since those were the most recent beans added, the first six beans removed are all red beans. Then at the end, all 10 of the green beans added on January 1 and two of the red beans added on January 2 are still remaining.

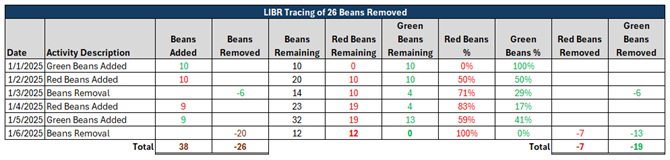

Lowest Intermediate Balance Rule (LIBR)

The LIBR method assumes the owner of commingled clean and unlawfully obtained assets will preserve the unlawfully obtained assets for the benefit of the victim. Therefore, the tainted assets are only considered to be used when the balance of the untainted assets is reduced to zero.

For the below LIBR example, you will see there are 10 green beans available when the first six beans are removed, which makes those six beans green. It is not until all green beans are removed that red beans begin to be pulled.

Pro Rata Distribution

The Pro Rata Distribution method assumes that the proportionate allocation of commingled tainted and untainted assets determines how much of assets removed is proportionally allocated to tainted and/or untainted assets.

For this Pro Rata Distribution example, you will see there are an equal number of red and green beans when the first removal of six beans occurs, making those six beans half red and half green. Then, the removal of 20 beans on January 6 occurred when the proportion of red and green beans were equal again, so the beans were equally removed between red and green again.

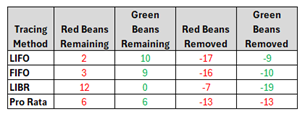

Comparison Across Models

The timing and extent of tainted and untainted assets added and removed drive which method results in higher concentrations of tainted or untainted assets as having been removed and that remain across these four tracing methods. The LIBR method will typically result in the least amount of tainted assets having been removed and the highest amount of tainted assets remaining, though.

The green and red beans specific fact pattern leveraged for the above examples resulted in the least remaining and most removed red beans under the LIFO method and the most remaining and least removed red beans under the LIBR method. The summary results are shown in the below chart:

As shown, the results can vary significantly across methods. Case-specific facts and circumstances should influence the decision of which method is most appropriate to achieve a fair and equitable results.

If you have a need for a “red and green bean counter” to trace commingled tainted and untainted assets or a related expert witness, contact James Rumph in our Columbus office or Tom Pratt and Brian Webster in Pittsburgh.

About Schneider Downs Business Advisory

Our experienced team of business advisors consisting of Certified Fraud Examiners, Certified in Valuation Analysts and Certified Mergers and Acquisition Advisors leverages its industry expertise to maximize value and minimize risk proactively or during acquisitions, litigation, arbitration, corporate reorganization and other major business events. To learn more, visit our dedicated Business Advisory page.