Typically, economic stimulus is intentional action by the government to encourage private sector economic activity. Economic stimulus within the United States may come in the form of monetary policy carried out by the Federal Reserve via lowering interest rates or quantitative easing. Congress can sometimes also provide a jump-start to the economy via fiscal policy, with lawmakers directing tax policies and government spending toward areas that they believe will boost the economy.

In March 2020, at the height of the COVID-19 pandemic, the U.S. government unveiled a bazooka of an economic stimulus package to help get America through the rest of the pandemic. Stimulus was provided through many measures; the Federal Reserve lowered interest rates to near 0 while at the same time providing much needed liquidity for capital markets through its asset purchase program (Quantitative Easing (QE)). The Fed also created specific lines of credit and programs to finance loans in order to keep debt markets open. Trillions of dollars of fiscal stimulus were provided by the U.S. government via the CARES Act and Consolidated Appropriations Act, among others. The capital markets response? The SP500 returned over 18% for the year 2020, a year impacted by a once in a lifetime pandemic and where U.S. unemployment hit almost 15%. The SP500 finished the year up almost 63% off the March lows.

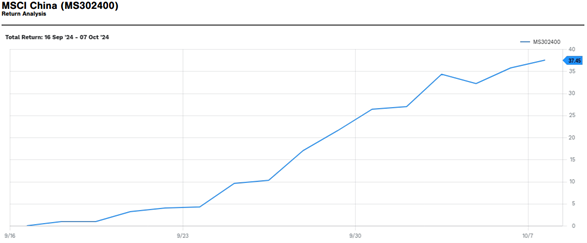

Recently, after a rather uninspiring 2024, the government of China decided that in order to get their economy into gear, it could use a little help from the public sector via an economic stimulus blitz. China’s central bank unveiled its biggest stimulus package since the pandemic in order to pull the economy back towards the government’s growth target. The People’s Bank of China (PBOC) announced it was cutting interest rates, reducing reserve requirements, and giving the property market direct support, among other things. Just three weeks after the People’s Bank of China announced new rounds of stimulus to jumpstart their economy, the Chinese stock market has returned over 37 percent (as of October 7th, 2024).

MSCI China +37.45% Total Return 9/16/2024 – 10/7/2024

Source: FactSet

There will be an academic argument for years to come on whether the economic stimulus that was flushed into capital markets in 2020 was excessive or not. The question can be asked whether or not throwing money at the world’s problems is a truly effective way to solve them, but one thing that cannot be questioned is whether or not government stimulus has an impact on economies and, more specifically, capital markets. One question does surface from this discussion: what happens when money can’t solve the problem?

About Schneider Wealth Management

Schneider Downs Wealth Management has been providing investment and retirement services since 2000. Although our service platforms continue to evolve, commitment to our clients remains our first priority. Our service is tailored to your individualized goals but built on the fundamental principles of our practice: fiduciary guidance, fee transparency and goal-based decision making. To learn more, visit our dedicated Wealth Management page.

Schneider Downs Wealth Management Advisors, LP (SDWMA) is a registered investment adviser with the U.S. Securities and Exchange Commission (SEC). SDWMA provides fee-based investment management services and financial planning services, along with fee-based retirement advisory and consulting services. Material discussed is meant for informational purposes only, and it is not to be construed as investment, tax or legal advice. Please note that individual situations can vary. Therefore, this information should be relied upon when coordinated with individual professional advice. Registration with the SEC does not imply any level of skill or training.