While much has been made of the negative headlines surrounding commercial real estate over the past two years, multifamily investments are poised to rebound in 2025 and beyond. After weathering an influx of new properties across the country and a difficult financing environment, apartments are now filling at a record pace as supply and demand come back into balance.

Post-Pandemic Challenges

Prior to COVID-19, multifamily lending was investor-friendly and widely available. Elevated transaction volumes in 2019 were driving values higher than ever, and stable rent growth created an environment for developers to increase production. The first quarter of 2020 saw a record number of apartment units start construction, then the pandemic hit and changed the real estate landscape across the country.

As supply chain issues delayed projects and office exposure threatened banks’ real estate lending capabilities, financing became more difficult. In 2022, the Federal Reserve started raising interest rates to combat inflation, and real estate transaction volumes began to drop. Properties that did sell transacted at markedly lower values.

In March of 2023, Signature Bank, which had allocated around $33.6 billion (45%) of its loans to commercial real estate, collapsed days after Silicon Valley Bank, igniting widespread concerns around loosening real estate underwriting standards. Amid heightened scrutiny, banks greatly cut back their lending, and traditional debt became a smaller proportionate share of capital in real estate transactions. This was particularly prevalent among the local and regional banks that had become a cornerstone of the commercial real estate debt market. Combined with rising rates, 2023 saw the most restrictive lending environment since the Great Recession.

Meanwhile, new apartments were being completed at the greatest pace in 40 years. From Q2 2023 to Q3 2024, 1.2 million units were delivered across the U.S., with the highest delivery numbers concentrated in the southeast and mountain west, where population growth was spurred by expanded remote work policies and business-friendly government. While demand remained strong, rent growth turned negative and transactions stalled, compounding financial issues for property owners nationwide. This left a number of operators unable to cover debt burdens that had sharply risen in prior quarters in conjunction with the Federal Reserve’s aggressive rate hikes. With the market in flux amid widespread uncertainty, transaction volumes had dropped to their lowest level in 10 years by Q1 2024.

The Current Market

Today, positive shifts in fundamental drivers of the multifamily investment space are leading to a brighter outlook. With supply and demand coming back into balance, debt markets loosening and transaction volumes rebounding, the reversals of multiple key negative trends observed over the past few years serve to bolster activity and pricing moving forward.

Positive Supply and Demand Trends

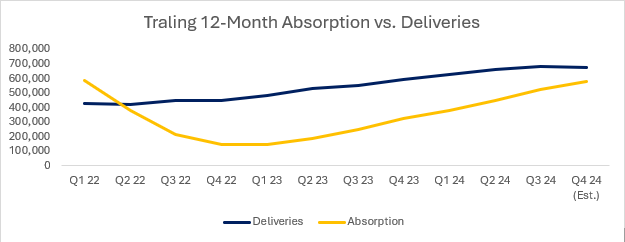

According to CoStar, apartment occupancy rates stabilized for the first time since 2021 last quarter, a key indicator that demand is catching up to supply. Absorption, the number of newly completed units rented, has been steadily increasing since 2022. This has closed the supply and demand gap significantly, a trend that may continue as CoStar estimates that new apartment deliveries peaked in Q3 2024. The narrowing difference between trailing 12-month absorption (demand) and trailing 12-month deliveries (supply) is illustrated below.

Source: CoStar Group

Perhaps more importantly, the pipeline of new multifamily projects is drying out. Q3 2024 construction starts reached their lowest level in over a decade, following six consecutive quarters of decreasing activity. CoStar estimates that 341K units will deliver in 2025, compared to 671K expected this year, followed by 270K and 269K in 2026 and 2027 respectively.

While high mortgage rates and a shortage of for-sale housing have kept some potential buyers in apartments for longer periods, there has also been an ongoing preference shift toward the flexibility and maintenance-free lifestyle of renting. According to a 2024 survey by property management software provider Entrata, 41% of renters say that their “American Dream” no longer has anything to do with homeownership, and 20% expect to be lifelong renters, a number that has increased by 33% since the 2021 survey. This demand is further bolstered by the increasing premium of buying versus renting for households across the country, which reached $1,030 per month as of mid-2023 according to John Burns Consulting.

The downturn in supply, combined with robust demand and shifting renter preferences, creates an environment for property owners to begin raising rents again in 2025.

Financing Availability and Transaction Volumes Increasing

Other factors are trending in a positive direction as well. Debt for multifamily has become more accessible. The National Multifamily Housing Council’s Q3 Survey of Apartment Conditions indicated a Debt Financing Index at its highest level since Q2 of 2019, indicating that lenders are more willing to originate loans and take on a greater proportionate share of capital in a given property. The Federal Reserve has cut rates as well, indicating that interest costs will continue to become more affordable as rates on commercial real estate loans move in response.

Sales volume is also ticking upwards, and values are improving. Many major markets in the south and west that were particularly impacted by oversupply are recovering. Tampa, Charlotte, Denver, Nashville and Las Vegas are among the many metro areas that have seen year-over-year apartment sales volume grow in 2024. This trend is on track to continue, as CoStar reports 116K units currently listed for sale in the U.S., a 433% increase from last November. Transactions are generating more liquidity in the market, which helps to establish fair values, creating stability in the near term and contributing to value growth in the coming years.

2025 and Beyond

Moving forward, negative trend reversals and positive political and regulatory tailwinds are on track to bolster the multifamily real estate market by increasing transaction activity and values.

As supply and demand rebalance, further rent growth may be achieved in markets that have seen zero to negative rent growth over the past couple years. This increase to bottom-line revenue, coupled with broader availability of more attractive financing options and terms, can expand transaction activity and drive exit values across the asset class.

Additionally, the results of the recent presidential election are likely to extend favorable real estate programs like Qualified Opportunity Zone investing and capital gains tax treatments, leading to more capital moving toward the sector as other asset classes continue to reach all-time highs and offer lower risk-adjusted returns relative to multifamily real estate.

It’s unlikely that lending availability and interest rates will return to pre-pandemic levels, but stability in the debt market will help to form a “new normal” in financing expectations. While banks still provide the majority of commercial real estate financing, a larger proportion of loans now come from private capital providers, a fundamental shift from pre-pandemic norms that is altering the makeup of the market while bolstering the availability of funding for multifamily investments. This is evidenced by a recent report by CBRE noting that banks share of non-agency loan closing in Q3 2024 was down 38% from their share a year earlier. Instead, CBRE observes alternative lenders – including life companies, debt funds and mortgage REITs – seizing heightened CRE lending market shares. In turn, these trends can lead to higher transaction volumes and mitigate some of the variability in projecting investment returns.

While we’re coming out of a challenging environment for multifamily real estate investing, we at Schneider Downs believe the future is bright, and we’re committed to providing the best available opportunities for investors to capitalize on this rebound. We will continue to monitor the national landscape and provide investment opportunities across the U.S., with a focus on active asset management and strengthening our long-standing industry partnerships.

About Schneider Downs Corporate Finance

Schneider Downs Corporate Finance (SDCF) is a FINRA-registered broker dealer dedicated to providing clients with profitable real estate investment opportunities. Since 2014, SDCF has placed over $237 million of equity in investments across the U.S. and has built deep relationships with a variety of respected multifamily developers and operators. To learn about investing with Schneider Downs, or for more information, contact [email protected].