Unless you’re new to the accounting industry, chances are you’ve heard phrases like “606” or “Rev Rec” a lot in recent years as references to the FASB’s major overhaul of accounting guidance for revenue recognition.

The much ballyhooed standard was issued in 2014, after many years of development, and finally became effective in 2018 for public companies and 2019 for private companies. Thankfully, with a few exceptions, the adoption of the new rules did not significantly alter the legacy accounting for most contractors, but one particular aspect of 606 has caused a fair amount of confusion in the last handful of years.

One of the stated objectives of the FASB’s Revenue Recognition project was to improve “comparability of revenue recognition practices across entities, industries, jurisdictions and capital markets.” In other words, the FASB intended to make it easier for users of the financial statements to compare companies.

Ironically, those rules created significant diversity in practice related to a common item in the construction industry – retainage. “Retainage” or “retention” receivables represent amounts the customer can contractually withhold from the consideration billed until certain project milestones are met or the project is completed. The retention portion of each invoice is typically paid at a later date than the remainder of the invoice that is typically considered trade receivable. Prior to the adoption of the new rules, most contractors presented retainage as a component of accounts receivable on the balance sheet, but the adoption of the new rules caused some contractors to consider retainage to fall under the newly created “contract asset.”

Understanding Contract Assets, Liabilities, and Receivables Under ASC 606

A contract asset is defined as an entity’s right to consideration in exchange for goods or services that the entity has transferred to a customer when that right is conditioned on something other than the passage of time (e.g., the entity’s future performance). Conversely, a contract liability is defined as an entity’s obligation to transfer goods or services to a customer for which the entity has received consideration from the customer.

Under current guidance, a receivable is defined as being a right to consideration that is not conditional upon anything other than the passage of time (i.e. “unconditional”). If a balance is subject to conditions other than passage of time, such as future performance or achievement of stated milestones, that balance should be reflected as a contract asset instead of a receivable (i.e. “conditional”).

The Challenges of Conditional Retainage and the PCC’s Response

The complication with conditional retainage is that each contract can only have one contract asset or liability balance, and almost all contracts already have a contract asset or liability in the form of an underbilling or overbilling. As a result, contracts with conditional retainage that are underbilled show a cumulative contract asset balance equal to the sum of the two, while contracts with conditional retainage that are underbilled show a net liability or asset. Various example scenarios are depicted in the example calculations below:

| Contract #1 | Contract #2 | Contract #3 | ||

| Revenue Recognized | $1,000,000 | $1,000,000 | $1,000,000 | |

| Amount Billed | $950,000 | $1,050,000 | $1,200,000 | |

| Underbilling / (Overbilling) | $50,000 | ($50,000) | ($200,000) | |

| Conditional Retainage | $95,000 | $105,000 | $120,000 | |

| Contract Asset / (Liability) | $145,000 | $55,000 | ($80,000) |

Conclusions on whether retainage is unconditional or conditional have varied from company to company. As a result, many users of financial statements have been left confused and struggling to find the legacy balances they considered to be meaningful. In September 2023, the topic was raised to the FASB’s Private Company Council (PCC) and it was officially added to the PCC’s docket in 2024. The PCC explored the issue and evaluated a number of presentation alternatives, notably alternatives that would have eliminated the netting effect of conditional retainage and overbillings.

After outreach and deliberation, the PCC ultimately decided that this issue did not warrant standard setting and that much of the diversity is the result of misunderstanding of, or disagreement with, the current rules. Further, the PCC believes existing disclosure templates, like the AICPA’s example financial statements for contractors, would provide financial statements users with the desired information. As a result, the PCC instructed the FASB to release an educational paper and removed this topic from its agenda in March 2025, thus dashing the hopes of those who wanted to see the presentation revert back to the pre-606 version and those hoping for presentation alternative to show contract assets and liabilities gross versus net.

Disclosure Requirements Surrounding Contract Assets and Liabilities

The FASB’s educational paper, released in April, focused primarily on current disclosure requirements surrounding contract assets and liabilities, and provided two example templates meant to satisfy feedback from users, particularly sureties.

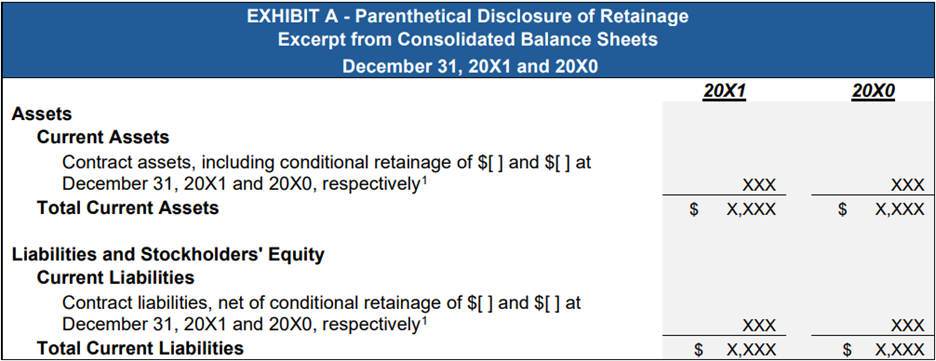

The first example displays parenthetical disclosure of conditional retainage within contract assets and contract liabilities on the balance sheet. This aligns with the AICPA’s example financial statements and allows users to calculate underbillings and overbillings by removing the effects of the conditional retainage amounts included in the parenthetical disclosure.

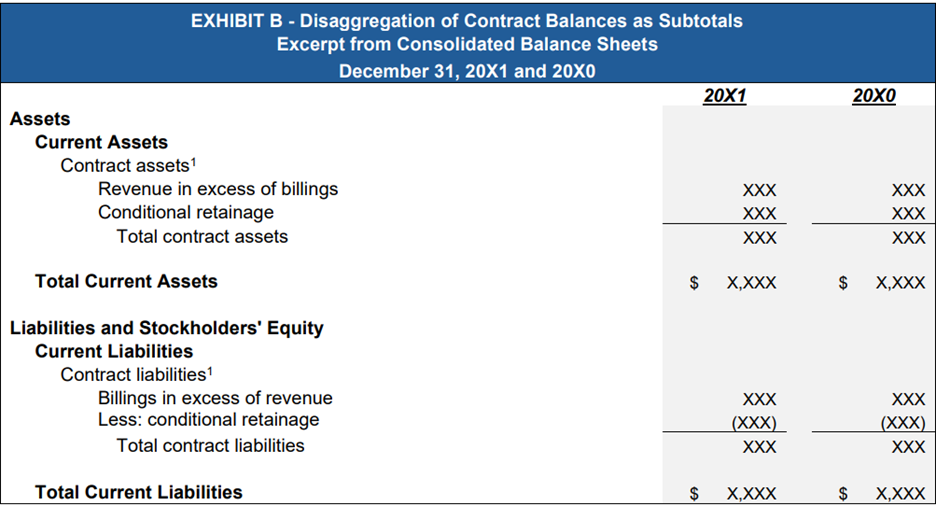

The second example displays disaggregated disclosure of conditional retainage with contract assets and contract liabilities on the balance sheet. In this example, the composition of contract asset and liability balances are broken out directly in the balance sheet.

The FASB is asking companies to revisit the existing guidance and rethink financial statement presentation. With the recent overhaul of the revenue recognition rules and the intent to eliminate industry-specific guidance, it’s not surprising the construction industry wasn’t provided with a carveout. For now, companies will need to make sure they’re evaluating the appropriate accounting for conditional retainage and working with users of their financial statements to ensure they’re providing meaningful transparency that adheres to the disclosure requirements.

About Schneider Downs Audit and Assurance Services

Schneider Downs’ engagement teams are hand-selected by our shareholders based on skill sets and experience and are available around the clock for consultation. Each attestation engagement is subject to our comprehensive quality control and risk management system, providing an independent review of audit opinions, related financial statements and significant underlying working papers, to ensure that the highest levels of professional standards are met.

To learn more, visit our dedicated Audit and Assurance page.