This article was co-authored by Megan Whitlock, Schneider Downs, and James McKinney, President, McKinney Properties.

Private real estate investments have long been favored among investors due to their potential for generating stable cash flow, inflation protection, and capital appreciation. Beyond these benefits, real estate investments offer significant tax advantages, which can enhance overall investor returns. This paper explores the tax efficiency and benefits of investing in private real estate, focusing on the impacts of depreciation, tax deferral, and long-term capital gains, with an overview of the differences for passive versus active investors. For the sake of simplicity, this article solely focuses on federal taxation consequences. Depending on the state where you reside and the state where the property is located, there may be similarities and differences between benefits at the state level and federal level.

Key Considerations

- Real Estate (RE) Investments may provide greater tax efficiency than other, more traditional forms of investment.

- Due to the tax shelter provided by depreciation, RE Investments have the ability to generate positive cash flow without taxable income in the early years of ownership.

- For an investor in the highest individual marginal tax rate, a (taxable) bond investment would have to generate a pre-tax yield of 9.52% to produce the same after-tax yield as a RE Investment with a pre-tax yield of 6.00%.

- For active investors and passive investors with outside passive income, the ability to use losses from a RE Investment to offset taxable income from other activities maximizes the depreciation deduction by further reducing the investor’s taxable income that year.

Depreciation: An Overview

Depreciation is the recognition of the physical wear and tear, or depletion, of real property over time, and it is an important tax benefit for real estate investors. Investors are permitted to deduct the cost of this physical depreciation on their property over a specified period, thereby reducing taxable income. The Internal Revenue Service (IRS) permits depreciation of residential real properties over 27.5 years and commercial real properties over 39 years under Internal Revenue Code (IRC) Section 1250. This non-cash deduction can significantly lower an investor’s annual tax liability. The impact of depreciation can vary depending on whether the investor is classified as passive or active.

Accelerated & Bonus Depreciation

The IRS also recognizes that specific components of a building, such as appliances, light fixtures, and cabinetry, have a shorter useful life than the structure of the building itself. These components are permitted to be depreciated over shorter useful lives of five years, seven years, or fifteen years, resulting in ‘accelerated’ depreciation under IRC Section 1245. Additionally, the Tax Cuts and Jobs Act of 2017 allows new owners of property placed in service in 2024 to depreciate 60% of the components of their building with a useful life of less than 20 years in the first year of ownership using bonus depreciation.

Accelerated and bonus depreciation each significantly reduces taxable income in the early years of ownership and can generate significant (tax) losses that may be used to offset other income for those investors that can use the losses.

Passive vs. Active Investor: Key Differences

The distinction between passive and active investors is crucial in understanding the applicability and extent of tax benefits. Active investors who materially participate in the management of their properties or meet the IRS criteria of a ‘real estate professional,’ may utilize depreciation deductions and apply losses to offset other business income. Passive Investors, typically involved in real estate through limited partnerships, REITs, or syndications, enjoy many of the same benefits but may face stricter limitations on the use of their losses.

Rules for Passive Investors

Passive losses from real estate investments can only be used to offset passive income. Investors with passive losses from a RE Investment but without outside passive income that year will have their losses suspended. Investors don’t lose the ability to claim these losses but instead must wait to utilize their benefits in a future year. In subsequent years, these ‘trapped’ losses may be used to offset passive income from the current RE Investment when it eventually produces taxable income or to reduce their gain when the investment is sold. Suspended passive losses can also be applied to offset passive income from an investor’s other passive activities, including other real estate investments. Investors with enough passive income to use the entire loss each year, maximize the benefit of the depreciation deduction.

The Mechanics of Depreciation – Straight-Line Method

Depreciation is calculated based on the property’s adjusted basis, which includes the purchase price plus any capital improvements minus the land value (which is assumed not to depreciate). For instance, if an investor buys a residential property on January 1st for $20,000,000, with $4,000,000 allocated to land, the depreciable basis would be $16,000,000. Spread over 27.5 years using the Straight-Line (SL) Method results in an annual depreciation deduction of approximately $581,818, reducing taxable income by a corresponding amount.

If this residential property generated an annual operating cash flow of $500,000 before depreciation, and there was no additional capital improvement made that year or mortgage amortization, then the depreciation deduction would result in an $81,818 tax loss. Passive investors with no outside passive income would have received the $500,000 in cash flow and owe no tax but have the $81,818 loss suspended for use in future years. Passive Investors with outside passive income could use all or part of the loss to offset their passive income. Active investors are generally permitted to use the loss against other personal income.

Distributions Versus Taxable Income

There is often a misunderstanding between distributions (cash received) and taxable income. Part of the tax efficiency of private real estate is derived from this distinction. In the early years of owning a stabilized, leveraged RE Investment, it is typical for both active and passive investors to receive cash distributions but owe no tax. This is due to the ‘tax shelter’ provided by the depreciation deduction. Depreciation reduces the asset’s tax basis and the owner’s taxable income, often resulting in losses through the first five to seven years of ownership. The tradeoff is an increase in gain at the time of sale, generally referred to as depreciation recapture, but the investor receives two key benefits from the depreciation deduction. First, depreciation recapture taxes are deferred until the sale of the property. Second, when the taxes are eventually due, if ever, the investor benefits from paying those taxes at the lower federal recapture rate of 25% on Section 1250 recapture for real property versus their ordinary income rate of as high as 37%.

Long-Term Capital Gains Tax Rates

Investments in real estate held for more than a year benefit from favorable long-term capital gains tax rates. Unlike short-term gains taxed at ordinary income rates, long-term capital gains are taxed at reduced rates: 0%, 15%, or 20%, depending on the investor’s taxable income. This lower tax rate significantly enhances the after-tax returns of real estate investments held for the long term.

Impact of Long-Term Capital Gains on Returns

The difference in tax rates between short-term and long-term capital gains can be substantial. For example, an investor in the highest tax bracket would pay 37% on short-term gains compared to 20% on long-term gains. By holding properties for the long term, investors can benefit from a nearly 50% reduction in the tax rate, substantially increasing net returns.

After-Tax Comparison of Real Estate Versus Bonds (Fixed Income)

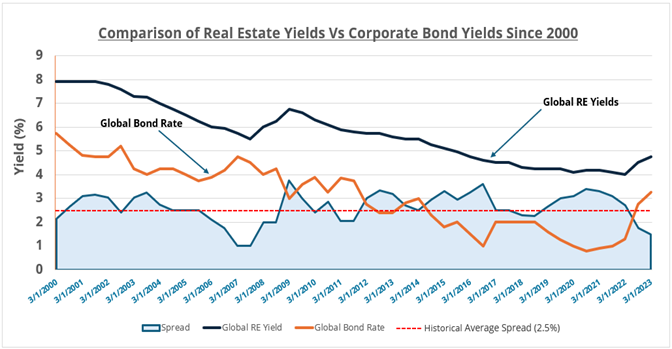

Bonds and real estate have a different risk/return profile. As the chart below shows, since 2000, the average annual yield produced by real estate has been roughly 250bp (2.50%) higher than the average yield on bonds globally.

Putting aside this difference, bonds are often compared to real estate investments for their ability to produce yield (i.e., cash flow). However, real estate investments offer distinct tax advantages compared to bonds due to the benefits of the depreciation deduction and capital gains treatment.

As mentioned above, the losses created by depreciation can offset all of the cash flow of a real estate investment for an extended period of time. As a result, after-tax yields equal pre-tax yields during this period. When sold, assuming a holding period of at least one year, the appreciation of the RE Investment is taxed as a long-term capital gain rather than as ordinary income.

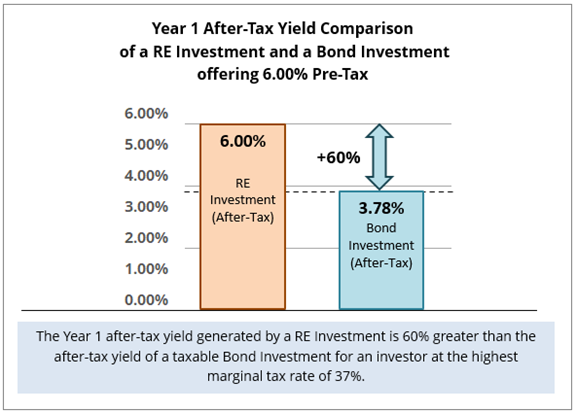

Conversely, the cash flow from bond investments is considered interest income payments, which are generally taxed as ordinary income at the investor’s marginal tax rate rather than as capital gains. While bonds provide a steady income stream, the annual after-tax yield is significantly reduced by the payment of income taxes, making it much less tax-efficient than a RE Investment. In Year 1 of a RE Investment, an investor at the highest marginal rate would earn a 60% higher after-tax yield than on a bond investment earning the same 6.00%.

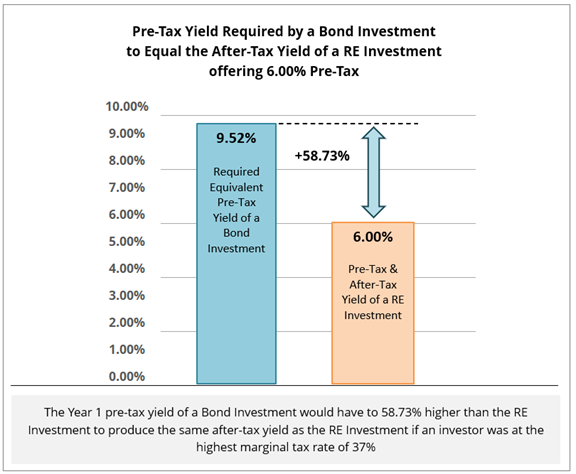

Looked at another way, for a bond investment to produce the same after-tax yield as a RE Investment, the bond investment would have to offer a significantly higher pre-tax yield. For an investor at the highest marginal tax rate of 37%, a bond investment would have to provide a pre-tax yield roughly 58% higher than a RE Investment to produce the equivalent after-tax yield.

Assuming straight-line depreciation, a 10-year holding period, and a 3% average annual appreciation, the blended annual tax rate for a RE Investment would be approximately 22.5%, with nearly all of this tax due at the time of sale rather than annually. This compares to an average annual tax rate of 37% for a bond investor at the highest marginal tax rate. Not only are the total taxes paid 40% less overall, but the deferral of the taxes until the end of the holding period creates a massive advantage in the time value of the tax payments, resulting in a much higher internal rate of return (IRR) for the investor. In addition, investors able to use the passive losses during the holding period, rather than having them suspended, would receive an even greater tax benefit.

Combining Tax Benefits for Optimal Tax Efficiency

When combined, depreciation, tax deferral, and long-term capital gains rates create a powerful framework for tax-efficient investing in real estate. Depreciation reduces annual taxable income, tax deferral postpones tax payments and maximizes reinvestment capital, and favorable capital gains rates reduce the overall tax burden on profits from property sales.

Other Tax Advantages

While not the subject of this article, real estate provides the opportunity to defer taxes in the future through a 1031 Exchange named after Section 1031 of the Internal Revenue Code. This provision allows investors to defer capital gains taxes by reinvesting the proceeds from the sale of real property into another real property of like-kind. Active and passive investors can benefit from 1031 exchanges, though active investors may have more control over the timing and management of the transactions. While the deferral of taxes through a 1031 Exchange can be a significant benefit to investors, the performance of the subsequent investment ultimately determines the deferral’s overall value.

Conclusion

Private real estate investment offers numerous tax advantages that can enhance overall returns and enable the investor to retain a majority of the cash flow that is distributed. Depreciation provides a valuable annual deduction, tax deferral preserves capital for reinvestment, and favorable long-term capital gains rates reduce the tax burden on profits. By leveraging these benefits, both active and passive Investors can achieve significant tax efficiency, making real estate a compelling investment choice. However, navigating the complexities and requirements of these tax provisions is essential to realize their full potential. Active investors, with greater involvement, may maximize these benefits more effectively, while passive investors should rely on skilled management and professional advice to optimize their returns.

About Schneider Downs Tax Services

Schneider Downs’ tax advisors have experience and expertise in a wide range of industries, including Automotive, Construction, Real Estate, Manufacturing, Energy & Resources, Higher Education, Not-for-profits, Transportation and others. Our industry knowledge and focus ensure the delivery of technical tax strategies that can be implemented as practical business initiatives.

To learn more, visit our dedicated Tax Services page.