Despite the down December, the S&P 500 ended 2024 with a 25% return for the year, delivering investors strong back-to-back annual returns in 2023 and 2024 – the first time in a quarter-century that the S&P 500 generated 25%+ returns in consecutive years (over a 57% total return in the last 2 years!). Of course, none of this would have been possible without the help of the illustrious “Magnificent 7” stocks (NVIDIA, Amazon, Tesla, Apple, Meta, Microsoft, and Alphabet/Google). But, from a return standpoint, were the Magnificent 7 really the best in breed?

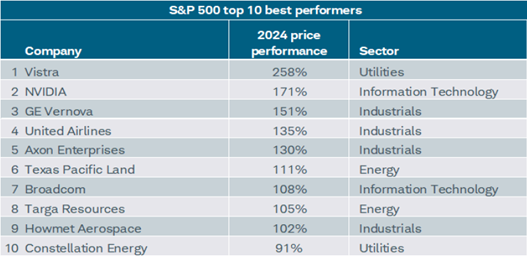

With all of the narrative within the financial news world that the Magnificent 7 are the best and brightest of the S&P 500, it may be difficult to hear that they, as a group, were not the best performers in 2024 from a price-return perspective. Only NVIDIA was in the top 10 S&P 500 performers for 2024, and it was not even the top name. Microsoft actually underperformed the S&P 500 for the year. Within the NASDAQ, none of the Mag 7 were in the top 10. Groups of stocks like the Mag 7 and other mega-cap names do represent an outsized contribution to the overall return of the S&P 500. However, this is not necessarily due to their returns being the best. The bloated weight in their contribution is partly due to the size of the companies. The S&P 500 is a market-cap-weighted index, meaning that the larger the company, the larger the contribution. Yes, companies have to grow in order to get quite big, but once they get to the top of the mountain, their contribution is reinforced.

There is an old saying about market breadth, “that the market is strongest when the soldiers, and not just the generals, are at the front line.” For 2024, only 19% of the stocks within the S&P 500 outperformed the index, but this improved over the last 4 months of the year with 40% of the stocks in the index having outperformed in the final 4 months. As market breadth continues to expand and the other 493 stocks in the index catch up to the Mag 7, U.S. large cap equities as a whole should be in a much healthier spot. Eventually, extreme style and/or size return differentials in the equity markets have reversed over time. While it is not clear if the mega-cap stock influence in the market will continue in 2025, it does seem reasonable to expect the average stock to begin outperforming the index at some point in 2025 or 2026.

If you have questions, please do not hesitate to contact our SD Wealth Management team at [email protected]

Schneider Downs Wealth Management Advisors, LP (SDWMA) is a registered investment adviser with the U.S. Securities and Exchange Commission (SEC). SDWMA provides fee-based investment management services and financial planning services, along with fee-based retirement advisory and consulting services. Material discussed is meant for informational purposes only, and it is not to be construed as investment, tax or legal advice. Please note that individual situations can vary. Therefore, this information should be relied upon when coordinated with individual professional advice. Registration with the SEC does not imply any level of skill or training.

Source: Article: It Was A Very Good Year