When considering federal estate tax planning, one of the most common objectives of the planner is removing assets from the taxpayer’s taxable estate. Many of these techniques are predicated upon a taxpayer’s assets appreciating at a rate that exceeds the Applicable Federal Rates (AFRs). Generally, lower AFRs make many estate planning techniques more appealing.

The AFRs, which are published every month by the Internal Revenue Service (IRS) via a Revenue Ruling, provide a benchmark for the minimum amount of interest that must be charged on any covered transaction (i.e., most intra-family asset sales and loan transactions). Generally, a failure to charge a rate of interest at least equal to the AFR at the time of the transaction will jeopardize the integrity of the transaction.

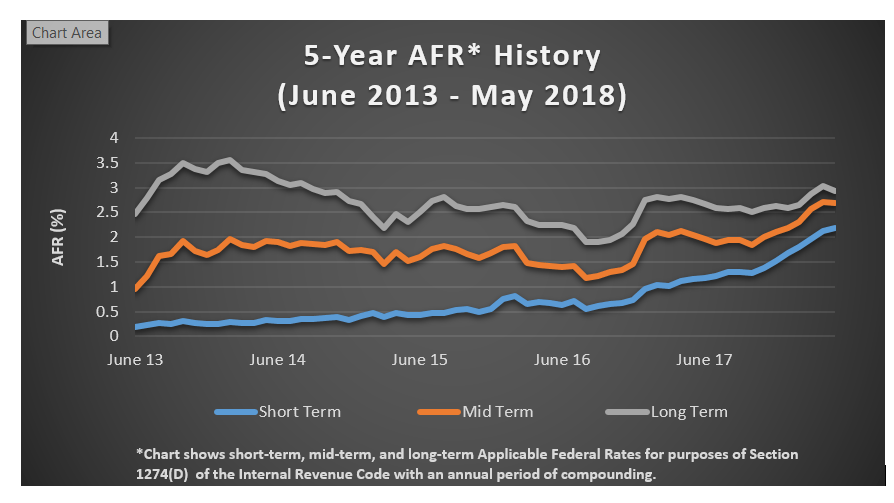

AFRs also play a critical role in determining which estate planning techniques to choose. For example, in 2007, the AFRs for all three term loan classifications (short-term, mid-term, and long-term) were hovering around 5%. Over the next six to seven years, AFRs plummeted to historic lows, with short- and mid-term rates falling under 1% and long-term rates falling under 2%. During this period, strategies that thrive on low AFRs such as Grantor Retain Annuity Trusts (GRATs), Charitable Lead Annuity Trusts (CLATs), and Intentionally Defective Grantor Trusts (IDGTs) were favored because they allowed the taxpayer to move significant assets out of his or her estate while only taking back into his or her estate an annuity/note payment calculated using these historically low AFRs.

However, since 2016 Q4, AFRs have been trending upward precipitously. As of May 2018, long-term rates were at their three-year high, mid-term rates were at their seven-year high, and short-term rates were at their ten-year high. Rising AFRs now mean that certain estate planning strategies that are more suitable for this environment are once again being considered and discussed. Mostly notably, consideration is now being given to implementing Qualified Personal Residence Trusts (QPRTs), Charitable Remainder Trusts (CRTs), and Grantor Retained Income Trusts (GRITs).

If you have not taken a look at your estate plan in a number of years, now may be the time to sit down and talk with a professional about how rising AFRs, not to mention new opportunities available pursuant to tax reform passed in December, 2017, can work in your advantage.